WHAT TO DO IN A DOWN MARKET?

“History provides a crucial insight regarding market crises: They are inevitable, painful, and ultimately surmountable.” ~Shelby M.C. Davis, founder and former mutual fund manager at Davis Selected Advisers

Investors who actively participated in the stock market following the Great Recession were fortunate to experience the longest-running bull market in history, starting on March 9, 2009.1

Unfortunately, as evidenced throughout history, bull runs always end at some point. The stock market itself has a natural life cycle that — like life itself — is destined to encounter peaks and valleys. Those scenarios frequently are preceded by events that impact market fundamentals or economic events, such as:

• Changes in interest rates

• New international trade negotiations, treaties and tariffs

• Fluctuating levels in the national debt

• Political controversies that impact national policies

• Global events that threaten economic stability

• Dramatic news headlines that shape investor sentiment

While each of these issues, and certainly all of them combined, generate cause for concern, it’s important to remember that we have been in similar circumstances before; we will be there again; and in between, we will experience more periods of economic and investment prosperity.

One way to help assuage market-related anxiety is to consider observations made by renowned investment experts who have weathered many market ups and downs over decades:2

INVESTMENT MARKETS GO THROUGH CYCLES

- A “market correction” is a decline of 10% or more

- A “bear market” is a decline of 20% or more

It is critical for investors to remember that what goes up inevitably comes down — at least where investment markets are concerned. Fluctuations are normal, and a decline in share prices offers the opportunity for investors to engage in a time-tested method for achieving more gains from well-established growth companies: buy low and sell high.

If companies — even steady, consistent growth performers — do not have the opportunity to reset prices, then investors would always have to buy at top-of-market prices to expand their position. However, when share prices drop, this is a window of opportunity to increase holdings in a reliable performer.

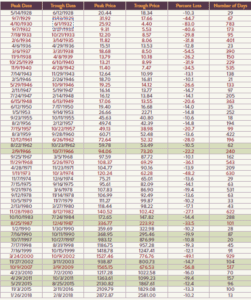

Another thing worth noting is that market corrections and bear markets are historically common, regular, and generally short-term. To illustrate this point, consider the table below, which depicts corrections and bear markets from 1928 to 2018 — noting the following points:

• Numbers in black denote a market correction

• Numbers in red denote a bear market

• Throughout this period, the S&P 500 experienced a correction or bear market every one to three years

• In those 90 years, there were only five time frames (highlighted) in which the index did not experience a correction or bear market for more than three years

S&P 500 CORRECTIONS & BEAR MARKETS SINCE 1928

DON’T DO ANYTHING DRASTIC

“A market downturn doesn’t bother us. It is an opportunity to increase our ownership of great companies with great management at good prices.” ~ Warren Buffett, chairman and CEO of Berkshire Hathaway

If you’re not interested in buying more shares during a market decline, then the key may be simply to hold fast. Focus on other elements of your financial plan that you can control, such as paying down debt or purchasing a life insurance policy to help provide long-term financial protection for your loved ones.

It is crucial to remember that investing is a long-term endeavor. The goal should be less about outperforming indexes and more about giving an investment uninterrupted time in the market — time to experience periods of rising prices and time to recover from periods of declining prices. After all, even short periods out of the market can have a substantial impact on investment returns.

FOLLOW YOUR PLAN: THIS IS WHY YOU HAVE IT

- 63% of a Sun Life Financial survey agreed that they worry less about money because they have a financial plan

- 73% of those respondents believe that financial planning has helped give them greater peace of mind

- And 2X more people with a financial plan are two times more likely to be confident in their plans to retire

One of the most important ways to help investors weather a down market is to have a financial plan already in place. There are many reasons for this. Establishing specific financial goals, a timeline for reaching those goals, an asset allocation strategy, and a carefully constructed portfolio are all significant components of a financial plan.

Some reasons people avoid consulting with a professional wealth manager to develop a plan are they don’t think they have enough assets to warrant a formal plan, they may believe they have a good grasp of their finances and/or they think it will be expensive or way too complicated.

However, setting aside all of those concerns, if you could achieve greater confidence in your investment strategy during a down market, that alone may be worth it to have a financial plan.

If you don’t have a financial plan, or even if you do but you’re feeling distressed over the current market environment, consult with a fiduciary financial advisor. These professionals have day-to-day experience working in investment markets and can share insights that may help you get through periods of uncertainty.

GENERAL GUIDELINES FOR DOWN MARKET MOVES

The garden-variety wisdom is generally to hunker down and maintain a long-term perspective when it comes to weathering a correction or bear market. However, with that said, there are some proactive things an investor can do to help protect and reinforce his financial position and mindset.

The following are some common recommendations.

Dollar-cost averaging

Investing the same amount of money on a regular basis can help smooth out the impact of fluctuating prices. With this tactic, called dollar-cost averaging, more shares are purchased at lower prices and fewer shares are purchased at higher prices. Over time, the investor pays less, on average, per share. However, be aware that regular investing doesn’t ensure a profit or protect against loss, and you need to consider whether you’re willing to continue investing when share prices are falling.

Diversify more

By spreading your money across a wider range of asset classes and sectors, you may be able to help reduce the impact of a market decline.

Consider a target-date fund

This type of fund comprises a mix of underlying stock and bond funds that gradually transfer to a more conservative allocation as the fund’s target date grows closer. Since the fund automatically adjusts to your established time frame, you can be less involved — and perhaps less stressed.

Consider your risk tolerance in relation to your goals

When it comes to investing, higher-risk holdings generally offer the potential for higher returns. The younger the investor, the more time he or she has to recoup any losses incurred through higher-risk investments. As investors grow older, they tend to be more conservative because they have less time to recover from market losses. However, much depends on how close you are to meeting your financial goals. Some individuals who are not well prepared for retirement may be willing to trade higher risk for the opportunity to accumulate more assets over a shorter period of time.

This is a scenario in which it is important to get advice from an experienced holistic financial advisor. He or she can determine an appropriate mix of investments to help meet an investor’s objectives without taking on undue risk.

TAKEAWAY: SHOULD A DOWN MARKET AFFECT YOU?

“Your success in investing will depend in part on your character and guts and in part on your ability to realize, at the height of ebullience and the depth of despair alike, that this, too, shall pass.”

~ Jack Bogle, founder and former chief executive of The Vanguard Group

Once you’ve considered all the variables, you may reach the conclusion shared by many of the most successful investors and market commentators — that down markets are not necessarily negative events. While they can be unnerving, it’s not always prudent to make changes to your portfolio.

A financial advisor can help walk you through the potential “what if” scenarios of a bear market or correction to help determine an appropriate investment strategy for your circumstances. For example, the closer you get to (or if you’re in) retirement, the more impact timing of negative returns can have on your long-financial goals. Factors such as future inflation and unknowable tax legislation also can impact your portfolio.

Financial advisors have experience working with these variables and helping clients both prepare for and weather down market cycles. If you have concerns or questions about the current market environment, contact Outlook Wealth Advisors for a complimentary consultation.

Award-winning CPAs and CFPs, the financial advisors at Outlook Wealth Advisors, offer a unique, holistic perspective most other firms simply cannot offer. They have assisted retirees and pre-retirees manage wealth and prepare tax-friendly retirement plans over 25 years. Email us at info@outlookwealth.com or call 281-872-1515 to get started.