DESIGNING YOUR FISCAL HOUSE TO WEATHER THE ELEMENTS

Building a strong, sustainable retirement income strategy is a lot like building a weather-resistant home. The overall strength of the house is dependent on how well its components (foundation, walls, floors, and roof) work together as a singular element. That has to be planned before you ever pick up a hammer. To build a home, you start with a full set of drawings—the blueprint. Likewise, a strong retirement strategy comprises a foundation, walls, roof, and even fencing.

One of the most important aspects of building your fiscal house is to include every element of your financial picture. It’s common for people to have their portfolio spread out among different strategies and with different professionals. However, to get your fiscal house in order, all these components need to be reviewed regularly and managed together as part of a total retirement strategy. You wouldn’t build a house with three different contractors each using different blueprints, and your fiscal house is no different. Here is a look at the different components of a weather-resistant fiscal house.

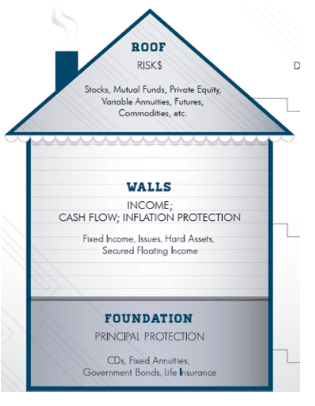

FOUNDATION

The foundation is the most important part. Without a foundation, you cannot have a house. If you have a problem with your foundation, it will damage every other part of your house as well. Financially speaking, the foundational elements of a retirement income strategy are typically the most protected assets. It’s money you can’t afford to lose.

Your foundation is the assets you need in order to pay your monthly expenses. These can include cash deposits in savings and checking accounts, certificates of deposit, government bonds, and traditional and fixed annuities. This is your starting point as you begin to build your fiscal house.

WALLS

Next, you build the walls. The walls of the retirement strategy are the first level of risk in a portfolio. They are important, but if they are damaged, the entire house won’t be destroyed; you will still be left with a strong foundation and the walls can be rebuilt over time. These assets can provide various benefits in your retirement portfolio, like income, cash flow, and inflation protection. Common wall holdings include corporate and municipal bonds, hard assets like gold, real estate, or mineral rights, and REITs. In addition to coordinating your walls with your foundation, it’s important that they coordinate with your roof as well.

ROOF

The roof of your fiscal house is represented by the highest risk level of your portfolio. Stocks, mutual funds, ETFs, options, and commodities make up your roof. These assets have the opportunity to grow, but they can also be lost due to external forces beyond your control—similar to the way a thunderstorm or hail could damage the roof of your home. Just like with your physical home, damage to your roof does not ruin your house. You only need to repair the damage to the roof to make your house whole again.

FENCING

Finally, as a means to help protect your future against portfolio losses that may occur before or after you die, it may be a good idea to build a fence around your fiscal house. Life insurance and annuities can be structured to help you replace your income or cover long-term care costs if needed. They can also be used to provide a guaranteed stream of income for your spouse after you pass away.

CHOOSING A BUILDER

An experienced builder has at their disposal the knowledge, skills, and tools to build a strong, weather-resistant home. Likewise, an independent financial advisor, like those at Outlook Wealth Advisors, will be able to help you develop the blueprint and deploy the proper holdings and asset allocation to build a market-resistant retirement income portfolio that optimizes income and mitigates taxes throughout your retirement. Email us at info@outlookwealth.com or call 281-872-1515 to get started.